Step-by-step import guide

When the Transition period ends on 31 December 2020, then UK & EU businesses will have to apply customs, excise and VAT procedures to goods traded between the UK & EU in the same way that already applies for goods exported to outside the EU. This step-by-step guide is intended to help businesses understand the key actions they will need to carry out in order to continue trading between the UK & EU from 1 January 2021. It is based on the existing guidance that already applies to the trade that EU and UK businesses carry out with businesses outside of the EU. The guide is for advice and guidance only and is not intended to cover all products and eventualities.

Some areas may change and businesses are advised to closely monitor relevant Government and Customs sources, many of which can be found in the useful links page.

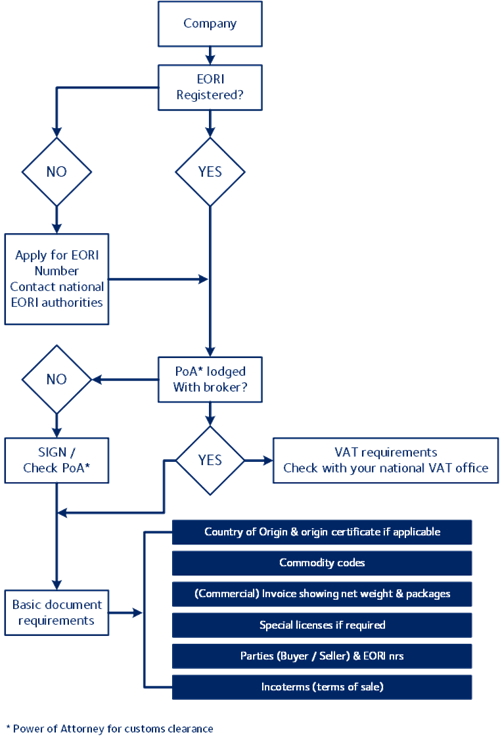

1) Register for an EORI number

You need an EORI number in order to trade, whether you are based in the UK or EU27. These are explained here. Your customers will need to register for an EU EORI number if they do not already have one. You can obtain an EORI number by registering with the Customs authority in your country.

2) Complete and send a Power of Attorney

DSV needs written authorisation from you to enable DSV to act as a Customs Agent on your behalf. This will apply to both Export Declarations and Import Clearances. Without this we cannot move your cargo through Customs. You can obtain these from your local DSV office.

3) Find out the commodity (HS classification) code of your goods

Commodity codes classify goods so you or your Broker can fill in import declarations.

Classifying your goods correctly means that you:

- Pay the correct amount of duty.

- Know if duty is suspended on any of your goods.

- Know if any preferential duty rates can be applied.

- Know if you need to obtain an import or export licence.

If you are unsure about how to classify your products, your national customs authority will have guides available online.

4) Determine the value of your goods

The value of the goods is necessary to determine the level of customs duty applicable. The value is also used for trade statistics. You arrive at the value of the goods by using one of six ways or ‘methods’. It is important to note that you must try Method 1 before going on to Method 2 and so on. Method 1 is based upon the transaction value. This is the price paid or payable by the buyer to the seller for the goods when sold for export in accordance with specific rules. These rules, along with the other methods of valuation, can be found in the World Trade Organization website here.

5) Check whether your goods are prohibited or restricted in any way or whether any additional requirements are necessary

There are some goods that you can’t bring into countries. Some goods are restricted, and you will need a special licence to import them. Licences are often needed for the import and export of military and para-military goods, dual-use and technology, artworks, plants and animals, medicines and chemicals. For more information, please see the current guidance on prohibited and restricted goods, Import and Export Licences on your local Customs or Government website.

6) Establish the origin of the goods

Establishing the origin of the goods will help to identify whether they qualify for lower or nil customs duty. There are two main categories of origin in the rules:

- Goods wholly obtained or produced in a single country

- Goods whose production involved materials from more than one country

The second category is more complex as there are several criteria to follow. Once you have clarified the origin of the goods, you can find out if they qualify for preferential treatment under a tariff preference scheme.

7) Consider whether you are eligible to use any facilitations

There are several of customs special procedures available to traders:

- Storage comprising of Customs Warehousing (CW)

- Specific use comprising of Temporary Admission and End Use

- Processing comprising Inward and Outward Processing

- Transit.

Before deciding whether to use a special procedure, you should research the procedure to make sure that you can meet all the obligations attached to it. To note, the use of special procedures requires prior authorisation from HMRC (UK) or local authorities in one of the 27 EU member states.

8) Declaring your import to customs

It is possible to make your own customs declarations, but the process is complicated and only suitable for more experienced importers. Most businesses use a customs broker or agent to do this for them. If DSV are handling your goods we can assist you with this. If you have decided to use a Customs Broker, you must, in a formal written authorisation, outline whether the broker is empowered to act as a ‘direct’ or ‘indirect’ representative. DSV can explain this and supply the necessary authorisation forms. If outsourcing customs to a 3rd party broker, it is important to inform DSV of this. Working with outsourced brokers can potentially result in additional delays in the process.

9) Pay duty on the goods

You might have to pay import duty depending on the classification of the goods and where they come from. Some goods benefit from a duty suspension regime. Information on this can be found on your national Customs website. Your goods might also be liable to additional duties, such as anti-dumping duties. Goods aren’t normally released by Customs until you’ve paid all the charges due. Exceptions to this include if the importer of the goods opens an account with Customs. Conditions must be met to take advantage of this scheme which will include providing guarantees.

You are required to keep records for all traded goods you declare to customs for the legally required period, typically 6-7 years, although this varies by country.

Customer import checklist in case of no-deal brexit